Table Of Content

- Capital Gains Tax Exclusion for Homeowners: What to Know

- Investment Exceptions

- Do Ottawa's proposed capital gains tax changes affect inherited properties?

- Income Tax: Selling jewellery to buy a house? You can claim exemption on capital gains

- Capital Gains Taxes on Property

- Estimated tax payments

- Business services

Finance Canada estimates the changes will affect about 40,000 individuals, but not everyone agrees that this tax change will only affect the wealthiest. It is vital that the property is bought either one year before or two years after the sale of jewellery. “Taxpayers can’t claim this exemption if they have more than one residential property.

Capital Gains Tax Exclusion for Homeowners: What to Know

There are a few ways to avoid the capital gains tax, but the big one is to stay put! The capital gains tax on your home sale depends on the amount of profit you make from the sale. Profit is generally defined as the difference between how much you paid for the home and how much you sold it for. If you sell your personal residence for less money than you paid for it, you can’t take a deduction for the capital loss. It’s considered to be a personal loss, and a capital loss from the sale of your residence does not reduce your income subject to tax. You pay capital gains tax only on the difference between what you sell the house for, and the amount it was worth when your last parent died.

Investment Exceptions

To determine if you meet the Eligibility Test or qualify for a partial exclusion, you will need to know the home's date of sale, meaning when you sold it. If you received Form 1099-S, Proceeds From Real Estate Transactions, the date of sale appears in box 1. If you didn’t receive Form 1099-S, the date of sale is either the date the title transferred or the date the economic burdens and benefits of ownership shifted to the buyer, whichever date is earlier.

Do Ottawa's proposed capital gains tax changes affect inherited properties?

Although we can’t respond individually to each comment received, we do appreciate your feedback and will consider your comments and suggestions as we revise our tax forms, instructions, and publications. Don’t send tax questions, tax returns, or payments to the above address. Extension of the exclusion of canceled or forgiven mortgage debt from income. The exclusion of income for mortgage debt canceled or forgiven was extended through December 31, 2025. The indebtedness discharged must generally be on a qualified principal residence, and based on an agreement in writing prior to January 1, 2026.

The Home Sale Tax Exemption - FindLaw

The Home Sale Tax Exemption.

Posted: Fri, 08 Sep 2023 07:00:00 GMT [source]

"I think the best thing to do is just to evaluate your assets and your net worth and determine if this is going to impact you," Rosen said. "If it's going to be a negative impact, consider your options and seek advice." "Those taxes are frankly the responsibility of the estate to pay, and then the person just takes over the asset. And they won't have that liability themselves," Weisleder said. One asset affected by these changes is real estate, including cottages and investment homes. Maximum limit of claiming income tax exemption under section 54F is ₹10 crore.

Income Tax: Selling jewellery to buy a house? You can claim exemption on capital gains

If your home substantially appreciated after you bought it, and you realized that appreciation when you sold it, you could have a sizable, taxable gain. Let's say that your cost basis in a duplex is $250,000 and that you've owned it for 10 years. Over the 10-year ownership period, you've claimed a total of $90,900 in depreciation expense. If you sell the property now for net proceeds of $350,000, you'll owe long-term capital gains tax on your $100,000 net profit plus depreciation recapture on $90,900, which is taxed at your marginal tax rate. Just like selling a primary residence, you can subtract the cost of improvements, real estate commissions, and closing costs from the gain you earned on your rental property.

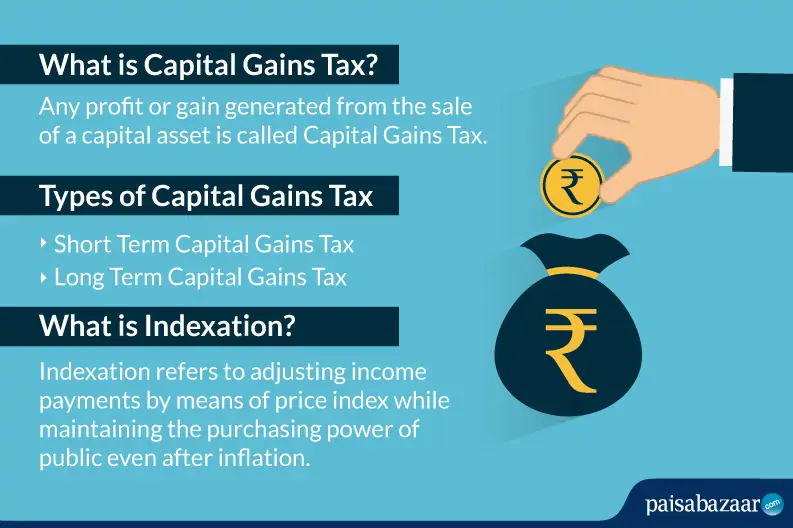

Capital Gains Taxes on Property

The maximum cap of claiming exemption is ₹10 crore, which was introduced in Budget 2023, prior to which — there was no such limit," he added. At base, such tactics obscure the fact that the higher rate is couched in a proposal within a proposal and, even then, would only apply to high earners. A financial advisor can help you manage your investment portfolio.

For taxable years beginning in 2023, the tax rate on most net capital gain is no higher than 15% for most individuals. To correctly arrive at your net capital gain or loss, capital gains and losses are classified as long-term or short-term. Generally, if you hold the asset for more than one year before you dispose of it, your capital gain or loss is long-term. If you hold it one year or less, your capital gain or loss is short-term.

Business services

However, a capital gains rate of 20% applies to the extent that your taxable income exceeds the thresholds set for the 15% capital gain rate. Fortunately, there are ways to avoid or reduce the capital gains tax on a home sale to keep as much profit in your pocket as possible. This tax break doesn't apply to main homes or vacation homes, but it can apply to rental real estate that you own. Gains from the sale of vacation homes don't qualify for the $250,000/$500,000 capital gains tax exclusion that applies to the sale of main homes. In essence, it's the government recapturing the savings you enjoyed due to the depreciation deduction.

The IRS’s commitment to LEP taxpayers is part of a multi-year timeline that began providing translations in 2023. You will continue to receive communications, including notices and letters, in English until they are translated to your preferred language. Payments of U.S. tax must be remitted to the IRS in U.S. dollars.

The debtor will be taxed on any remaining forgiven debt at ordinary income tax rates up to 37%. If you do have to pay capital gains tax, how much you owe will depend on how long you owned the house, your filing status, and your income. If you receive an informational income-reporting document such as Form 1099-S, Proceeds From Real Estate Transactions, you must report the sale of the home even if the gain from the sale is excludable. Additionally, you must report the sale of the home if you can't exclude all of your capital gain from income. Use Schedule D (Form 1040), Capital Gains and Losses and Form 8949, Sales and Other Dispositions of Capital Assets when required to report the home sale.

You're no longer middle-class if you own a cottage or investment property - The Globe and Mail

You're no longer middle-class if you own a cottage or investment property.

Posted: Fri, 26 Apr 2024 19:10:06 GMT [source]

The following are some assets that are and are not eligible. Did you know that you could donate appreciated stock instead of cash to your charity of choice? When you donate profitable investments to a charitable organization, you don’t have to pay capital gains tax, and usually, neither does the charity. You’ll also receive a tax deduction for your charitable donation.

In some cases, the IRS may require quarterly estimated tax payments. Though the actual tax may not be due for a while, you may incur penalties for having a large payment due without having made any installment payments towards. The capital gains tax effectively reduces the overall return generated by the investment. But there is a legitimate way for some investors to reduce or even eliminate their net capital gains taxes for the year. The deduction for depreciation essentially reduces the amount you're considered to have paid for the property in the first place. That in turn can increase your taxable capital gain if you sell the property.

You can get a transcript, review your most recently filed tax return, and get your adjusted gross income. If you did receive any federal mortgage subsidies, you must file Form 8828 with your tax return whether you sold your home at a loss or a gain. However, if you had a written agreement for the forgiveness of the debt in place before January 1, 2026, then you might be able to exclude the forgiven amount from your income. 4681, Canceled Debts, Foreclosures, Repossessions, and Abandonments.

For a step-by-step guide to determining whether your home sale qualifies for the maximum exclusion, see Does Your Home Sale Qualify for the Exclusion of Gain? The following example demonstrates separate calculations for business and residential uses. If you and your spouse owned the home either as tenants by the entirety or as joint tenants with right of survivorship, you will each be considered to have owned one-half of the home. Improvements add to the value of your home, prolong its useful life, or adapt it to new uses. You add the cost of additions and improvements to the basis of your property. The sale of a remainder interest in your home is eligible for the exclusion only if both of the following conditions are met.

If the mutual fund held the capital asset for more than one year, the nature of the income from a sale of the capital asset is capital gain, and the mutual fund passes it on to you as a capital gain distribution. These capital gain distributions are usually paid to you or credited to your mutual fund account, and are considered income to you. Form 1099-DIV, Dividends and Distributions distinguishes capital gain distributions from other types of income, such as ordinary dividends. So, if an investor whose annual income is $50,000 can, in the first year, report $50,000 minus a maximum annual claim of $3,000.

No comments:

Post a Comment